Introduction

I just got back from the annual J.P. Morgan (JPM) Healthcare Conference, which got me thinking about the tension between optimism and pessimism in our industry. That reminded me of a surprising insight from Andrew Ross Sorkin’s 1929: Inside the Greatest Crash in Wall Street History: even days before the market collapsed, strong optimists (bulls) and pessimists (bears) were making their case for the U.S. economy. Today, biopharma faces a similar dynamic, raising an important question: what are the bull vs. bear arguments for 2026? And what events could tip the balance?

In my view, there are four areas of U.S. biopharma to watch in 2026: scientific innovation, capital markets, China, and policy. For each, it’s a fascinating race between bull and bear arguments. Given my perch, I will spend this blog digging into the first three categories, as I am not a policy expert! But first, let’s discuss the overarching bull and bear cases in 2026.

What are the bull and bear arguments for U.S. biopharma in 2026?

I read Sorkin’s book at the end of 2025, while visiting my family for the holidays, which is why it was top of mind going into JPM. In the midst of reading the book, I reached out to colleagues and friends in biopharma for their perspective on bull vs. bear arguments in 2026. I also read published reports (here, here, here, here, here, here, here; my AI summary of analyst reports here) and re-watched Bruce Booth’s outstanding Year in Review (2025 video link here). I pressured tested my ideas during JPM and asked for input via LinkedIn. Those conversations and reports informed the perspective I share below – and what events to watch as the year unfolds.

The bull argument starts with unmet medical need. Just look around – there is a lot of room for improvement in the U.S. healthcare system, and pharmaceutical innovation is an important component that can drive progress. As an example, my mom was diagnosed in 2020 with triple negative breast cancer. I was surprised by the primitive nature of her chemo and radiation therapies, not to mention the rudimentary nature of follow-up surveillance. There must be a better way!

The bull arguments have their foundation in the fundamentals of our industry, which remain strong. The U.S. has the strongest academic institutions in the world, which serve as a source of new ideas and talent. Early-stage biotech companies continue to receive funding and serve as a source of innovative products. Multiple Big Pharma companies have innovative R&D pipelines and capital to continue to fuel the virtuous cycle of scientific innovation. And capital markets are on the rebound, with strong momentum coming out of the second half of 2025 (2H2025).

Thus, the crux of the bull argument is that there will be policy stabilization, continued flow of capital, continued scientific innovation across multiple dimensions, and a healthy – even if competitive – relationship with China.

The bear argument hinges on a mix of uncertainty and unmet expectations, which could impact our ability as an industry to innovate.

Now, let’s dig into the factors that could tip the scale.

1. Scientific innovation

The future of our industry hinges on our ability to continue to innovate in a way that is meaningful for patients. Scientific advancement is not a given; it takes continued investment (see my recent blog post on “blended innovation” here). There are two stories to follow. The first is AI (of course!). The second is clinical advancements that create new markets.

a. Artificial Intelligence (AI). The AI story in 2026 is not “AI discovers drugs overnight.” Rather, it’s whether AI can solve very specific problems along the R&D value chain. I will admit my biases upfront: I am a big believer in AI’s ability to improve R&D productivity over the long run. However, I am less sanguine about near-term breakthroughs that will “revolutionize” R&D productivity. I am playing the AI long-game in R&D – and I’m in good company (see here, here, here).

Why the AI long-game and not near-term revolution? I always go back to the five core principles of R&D productivity: causal human biology, matching modality to mechanism, path to clinical proof-of-concept, accelerated full development, and maximizing market access (here). There are dozens – if not hundreds – of steps for each of these five principles. For example, we are still a long way from reliably defining causal nodes of human biology, the starting point of any successful drug. We’ve made impressive progress in predictive molecule invention – including generative AI to expand chemical diversity and speed up the optimization of pharmaceutical properties. But implementation will take time, and the impact on R&D productivity will take even longer. In clinical development, AI has been shown to boost enrollment by 10–20%, compress timelines by around six months, and significantly reduce the cost of trial operations (McKinsey report here).

To that end, I have placed different R&D applications along the Gartner hype cycle curve (see Figure below), with an attempt to capture three dimensions of AI applications: maturity, transformational potential, and hype. The list is far from complete, and the graph has limitations that don’t capture the complexity of AI in biopharma. Moreover, I am sure many will disagree with the placements. Please let me know if there is a better way to present the three dimensions and if you disagree with the categorization…and why!

The near-term bull case is incremental improvements in R&D productivity. In Research, that means better selection of targets based on foundational models and faster cycle times to deliver development candidates (here, here). In Development, that means faster site selection, better enrollment, automated document drafting, improved signal detection in trials, and shorter cycle times per asset.

The bear case is that companies overinvest in AI at the expense of approaches that work today, and there is a paradoxical decrease in R&D productivity in the near-term.

What to watch: I want to see real R&D problems solved with AI and measurable gains in R&D productivity. As a biopharma industry, we need to shift from hype to action. To quote Rod Tidwell, “Show me the money!”

b. New markets. While AI gets all the attention, I think the more interesting near-term trend is whether science will create new and unexpected commercial markets. Remember: the first GLP1 was approved for diabetes in 2005 and for weight management in 2014, and it wasn’t until 2023 that the first in this class surpassed $1B in annual sales. New markets take time – but when they appear, they can change an industry (e.g., see a list of “human-made miracles” here).

What are the next new commercial markets? Here are a few to consider:

– treat-to-cure in chronic diseases such as autoimmunity (immune reset, here) and multiple myeloma;

– N-of-1 programmable therapeutics for genetic diseases (e.g., Baby KJ, here);

– neurodegenerative diseases such as Alzheimer’s disease, Parkinson’s disease, and Amyotrophic Lateral Sclerosis (ALS) – where there are few disease modifying therapies today;

– preventative therapies for chronic diseases such heart disease (e.g., long-acting treatments for dyslipidemias) or even cancer (see here , here, here for an example in blood cancers);

– novel tissue delivery mechanisms to broaden the impact of genetic medicines;

– new foundational therapies in oncology, which create new combination therapies that displace current standard of care (e.g., PD(L)1xVEGF replacing anti-PD(L)1 therapies); and

– novel mechanisms for sleep disturbances such as narcolepsy (e.g., orexin agonists; foundational models for sleep here).

The bull case is that advancements such as those above indeed start to create new commercial markets.

The bear case is that, well, new markets don’t appear!

What to watch: There are interesting trial readouts and regulatory decisions that will happen in 2026: see here, here, here. And, hey, you can always just ask AI!

2. Capital markets and deal-making

Biopharma capital markets rebounded in the second half of 2025, with public indices posting their strongest six-month stretch in a decade and private funding holding steady at healthy levels. While valuations remain historically low, follow-on financing gained traction, and even a slim IPO class outperformed prior years. Partnerships and M&A added to the momentum: licensing deals jumped ~40%, fueled by Asia-based collaborations, and public M&A hit $120B in upfront value, the highest in 20 years. All signs point to renewed confidence heading into 2026.

What do these numbers mean to the bull vs. bear race in 2026?

The most plausible scenario is the bull case: a reopening of IPOs for quality names, continued licensing and collaboration (perhaps with a shift towards early-stage deals), and continued M&A. Commentary from sector investors and capital-markets coverage has explicitly pointed to a 2026 pickup in IPO activity after a drought (links here, here; AI summary of analyst reports here), as well as to materially increased Big Pharma M&A value and a return of large deals. A recent Deloitte survey indicated that M&A remains high on the agenda of biopharma executives (here). Indeed, most of my conversations at JPM foreshadowed optimism!

The bear case is tied to policy uncertainty, a condition markets have historically struggled to price.

What to watch: There are fundamentals to track, just like every year: number and value of biopharma partnerships; number and pricing of IPOs, performance post-IPO, and follow-on financing; and number, value, and origin of M&A deals. Beyond the fundamentals, however, there are two specific categories that I want to track:

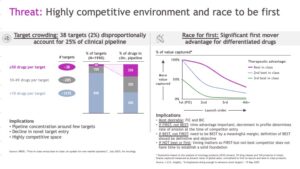

a. The first is target crowding (here, here, here, here), and how such crowding can drive up deal value and change the structure of partnerships. Here are some impactful numbers: As of 2025, approximately 25% of the entire global R&D pipeline (roughly 13,600 drug-target pairs) is focused on just 38 unique biological targets (see Figure below). Thirty-eight! The annual rate of novel biological targets entering the pipeline has plummeted from ~100 per year a decade ago to only 30 in 2024. Meanwhile, between 2000 and 2022, assets per target surged: from ~3 to ~7 overall, and in oncology from ~1.8 to ~9 (a >5× increase). This crowding is compressing time between launches; for example, for the top three oncology targets (HER2, CD20, BCR‑ABL) the “launch gap” shrank from 6.3 years (1st→2nd) to 2.4 years (2nd→3rd) and to ~1.4 years by the 5th launch.

Target crowding has major financial implications, especially related to Business Development (BD). First, BD teams are shifting from broad portfolio building to “fewer, higher value” deals focused on strategic differentiation. Second, overall deal values are rising, with deal structures becoming heavily back-ended (e.g., Contingent Value Rights and milestone-based payments) to manage the commercial uncertainty of entering crowded markets. Third, there is a move to clinical deals where biology has been de-risked (e.g., new modality X against pharmacologically validated target Y) and away from earlier-stage innovative discovery partnerships. With this shift, companies understand they will likely have to pay even more later for first and/or differentiated assets.

b. The second category to track is the recycling of capital outside of the U.S.– and China in particular. In 2025, there were ~150 biopharma China deals of all types – including licensings, acquisitions, and financings – which has been steady over the last few years but up 3x from ~50 deals in 2021. What has exploded is the value of those deals, from ~$30B in 2022 to ~$100B in 2025, representing ~40% of the total deal value in biopharma (up from ~13% in 2019; here). That is, the market has shifted from “more deals every year” to “still many deals, but value per deal rising sharply,” especially from 2023 to 2025.

What will the number and value of deals be in 2026, including as a percentage of all deals executed? More generally, what happens to the U.S. biotech market if there continues to be an increase in deal flow to Chinese-based companies? Is there a threshold at which U.S.-based VC and equity markets fail to benefit from capital recycling, thereby compromising the U.S.-system? How does that threshold vary by early-stage discovery VCs vs. clinical-staged investors? Do Chinese companies start to penetrate commercial markets previously dominated by non-Chinese multinational pharmaceutical companies (see “Rising Commercialization Challenges” section, page 8 from BCG report here)?

3. China

China was an important source of innovation in 2025; there is little doubt that will continue in 2026 (here).However, there are two important factors that could impact the U.S. biopharma industry: China’s regulatory reforms, which are aimed at speed and global integration, and U.S. scrutiny of foreign data integrity and biosecurity pathways. On the former, China has formalized pathways that allow for IND reviews in ~30 working days and encourage global synchronized development. On the latter, increased U.S. scrutiny of data integrity and biosecurity could result in a “regulatory chill,” affecting cross-border trials and increasing intellectual property (IP) risk.

The bull case is that U.S. biopharma can convert “China speed” into “U.S. execution plus global commercialization,” provided regulatory and geopolitical constraints don’t sever the bridge. This is a topic FDA Commissioner recently addressed during a JPM podcast interview (here). However, at some point this source of innovation becomes competition, and might even lead to disproportionate investment flowing into China and away from other countries.

The bear case is that China overtakes the U.S. as a source of innovation; the recycling of capital goes disproportionately to Chinese investment and biopharma companies, especially for early discovery innovation (see WSJ article here); and/or geopolitical tensions rise such that partnering with China is no longer an option for U.S. biopharma companies. If cross-border bridges narrow, U.S. companies face a lose-lose: China competes faster and becomes harder to partner with, raising pipeline scarcity and BD costs.

What to watch: The most critical metric is China’s share of global biopharma deal flow: licensing, partnerships, and M&A. Will U.S. regulators accept Chinese clinical data for trial design and approvals? Do regulatory agencies in other countries take a rigid or more permissive approach to clinical data generated in China? Does geopolitical tension rise to the point where partnerships become more challenging?

So who wins the U.S. biopharma race in 2026: the bull or bear?

It’s a close call. From where I sit, the bull has the edge over the bear. Looking at the three dimensions discussed above, here is what the world looks like if I’m right…and what it might look like if I’m wrong.

For the bull to win: science and markets continue their march forward, and the U.S. maintains its leadership position in biopharma, with China as a partner.

- Science continues its march forward. AI demonstrates near-term impact on operational aspects of R&D, with a few “wins” in other areas (i.e., movement in the positive direction along the hype cycle). Further, new markets emerge, providing new and unexpected sources of future revenue for the industry.

- Capital markets continue the momentum from 2H2025. The combination of improving M&A appetite and credible commentary around IPO re-opening suggests the liquidity “plumbing” may return sooner than expected.

- China as partner. A new equilibrium emerges with China, making partnerships with U.S. companies a win-win.

Why the bear has a fighting chance: AI is more hype than hit, capital markets freeze, and China’s biopharma industry surpasses the U.S. industry.

- Science buckles. AI is seen as hype. Clinical trial failures mount, especially for medicines predicted to open new commercial markets.

- Capital markets freeze. Interest rates rise, driven by inflation, which stifles biotech investment. M&A and partnership momentum slows, and generalists invest in other sectors. Big Pharma industry consolidation dominates deal flow, limiting capital recycling into VCs and SMID cap companies.

- China becomes the global biopharma leader. Rather than acting as a partner in the global biopharma ecosystem, China overtakes U.S. industry. Geopolitics and regulatory pressures increase.

Conclusions

I expect 2026 to be a dynamic year in biopharma. My prediction: a narrow bull win. The bull case outcome requires just enough stability – AI-driven productivity gains, accessible capital, and synergistic partnerships. The bear wins if uncertainty freezes capital markets and stifles innovation. In short, 2026 will test whether science and strategy can outrun volatility and unpredictability. The outcome could shape biopharma’s trajectory for years to come.

[ You can download a pdf of this blog here. ]